- The old-age dependency ratio in Europe is expected to roughly double by 2050. Yet only half of the general public express concern over the future costs of pensions.

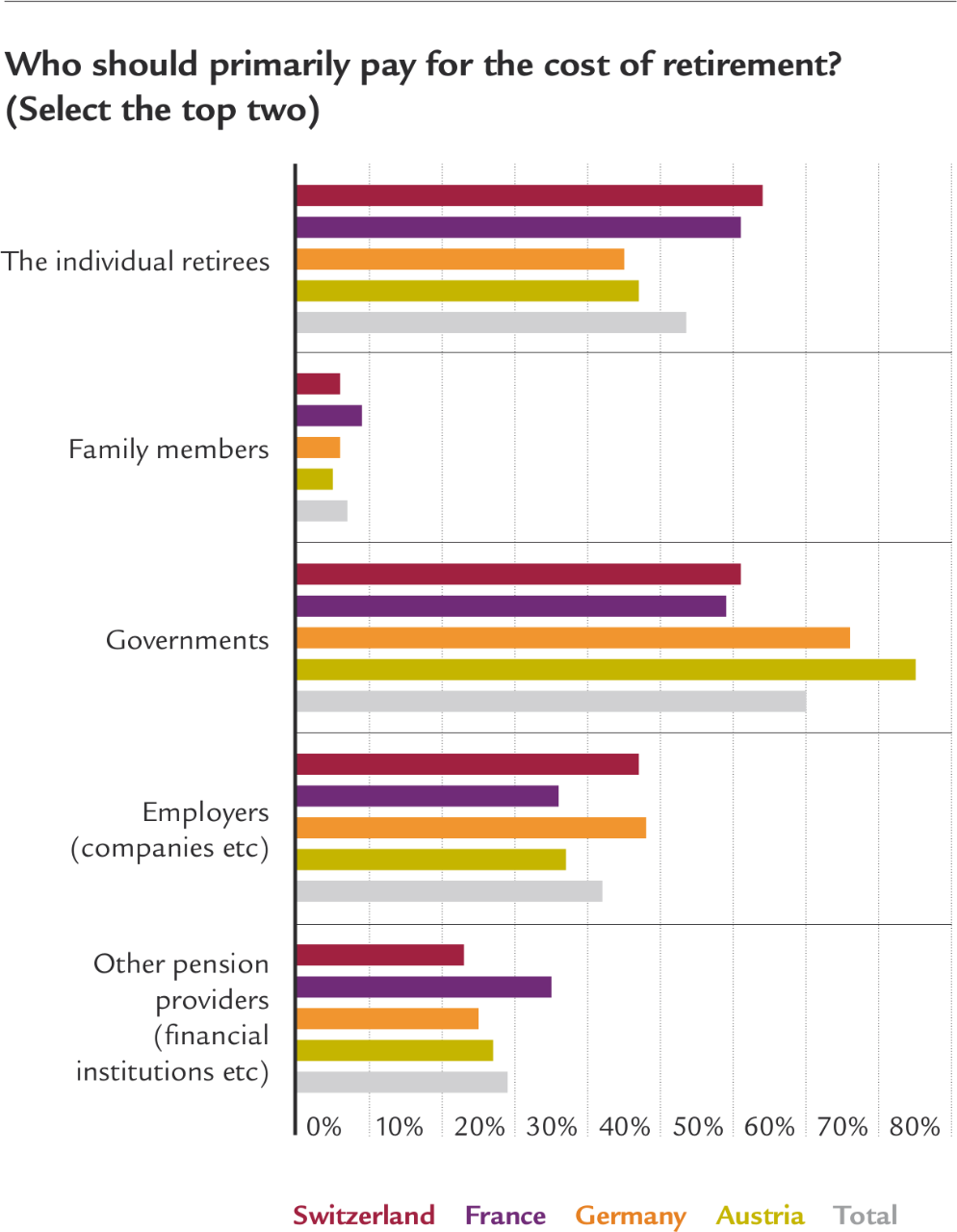

- More than three-quarters of individuals surveyed by The Economist Intelligence Unit (EIU) in Germany and Austria expect their government to cover the costs of their retirement. By contrast, over 60% of respondents in Switzerland and France believe that individual retirees should be responsible.

- More seniors could be enticed to stay in the workforce in their later years. But job cuts often target older workers while offering them few opportunities to retire gradually.

Changing demographics are putting pressure on social security systems across Europe. Many governments have responded by raising retirement ages and generally shifting saving and investment responsibilities to workers, leading to changes in the social contract. A longer working life is likely to be a key part of these shifts, although at present many workers have yet to be won over to this prospect.

February 15th 2015 was a special day for Saint-Priest, a small village in the Rhône-Alpes region of France: Thérèse Ladigue celebrated her 113th birthday and became the oldest person in France. Born when the first Ford Model A was produced in America, she was one of a small number of so-called supercentenarians (those who are at least 110 years old).

While supercentarians are likely to remain a small segment of the population in France—and in Europe in general—for the foreseeable future, increasing longevity will result in a dramatically older society with more over-65s and more over-80s, centenarians and supercentenarians. According to the EU, the share of the very old—defined as those aged 80 or over—is projected to more than double, rising from 26m very old persons in 2014 to 63.9m by 2080.

Will Europe’s citizens be caught unprepared?

These increases in life expectancy are a defining achievement of the last century. But what is good for the individual poses certain challenges for the state. Increased life expectancy, together with declining birth rates and in many countries retiring baby boomers, places significant pressure on pension systems across Europe.

The old-age dependency ratio, which in effect shows how many retired people a potential worker has to sustain, is expected to rise from 14.2% in 2012 to 34% by 2050. “With a smaller fraction of the population of working age and more people in old age, there is considerable pressure on European pension systems and public finances,” says Axel Börsch-Supan, director of the Munich Centre for the Economics of Ageing.

Surprisingly, in the face of these concerns, a sizable portion of the general public are unconcerned by these pension challenges. According to a recent EIU survey of over 1,200 people from Germany, France, Austria and Switzerland, only 50% of respondents feel that their countries are “not well prepared for higher pension costs”.

The question of who should pay differs among the respondents. At first glance, the overwhelming majority of respondents expect their government to bear this burden. But underneath this lie substantial nuances by country: over 60% of respondents in Switzerland and France say that individual retirees should bear the cost of retirement; this is roughly tied with those looking to government. By contrast, over three-quarters of respondents in Germany and Austria expect their government to cover these expenses, while under half look to the retirees themselves.

Are occupational pensions enough to fill any gaps left by governments? More than two-fifths of respondents in the survey believe that companies should provide primarily for the costs of retirement. This figure rises to nearly half in Switzerland and Germany. In France, on the other hand, barely over one-third (36%) look to employers, with similar numbers turning to other pension providers. It is clear that the social contract is in flux and that cultural differences will influence how these debates are resolved. Regardless of how the costs are shared, increasing longevity will require that citizens prepare for longer, healthier lives. This is likely to play out through a mix of increasing personal responsibility and changes to government policy.

Running backwards on retirement

Governments across Europe are aware of demographic change, and many are in the process of reforming their pension systems. This restructuring process has had varied results. Some countries have introduced penalties for workers retiring early (in Austria, for instance, your pension is reduced by 7% for every year you retire before 65); many countries have instituted benefits for working longer; and some, such as Sweden and Finland, have also focused on improving working conditions for older workers.

Pension reform can be challenging because of the transfer from one generation to the next. Inevitably, there are pressures to backpedal: France, for example, recently delayed planned reductions in its retirement age. The French government has said that the €3bn (US$3.34bn) annual costs will be met by a 0.1 percentage point rise in payroll charges. Germany, meanwhile, has lowered its retirement age from 65 to 63 for long-time workers.“

The reduction in the retirement age in Germany obviously goes in the wrong direction,” notes Professor Börsch-Supan. “It was a political decision, however; promises made before the recent election. Overall, we have had effective pension reforms in Germany over the last 10-15 years.”

2.7%Germany is expected to increase in pension expenditure by 2.7% GDP by 2060. This will make its pension expenditure one of the highest in Europe.

Out with the old, in with pension reforms

In general, pension reforms in the OECD “have helped greatly increase the sustainability of pension systems”, according to the OECD report Pensions at a Glance 2015. Indeed, the most recent projections of the EU’s Ageing Working Group foresee a stabilisation of public pension spending as a share of GDP between 2015 and 2060 for most European countries.

Projections can, however, mask differences across the EU. The 2015 Ageing Report by the European Commission shows that Germany, for example, expects an increase in pension expenditure of 2.7 percentage points of GDP from 10% to 12.7% over the period 2013-60. This overall increase will make pension expenditure one of the highest in Europe. France, on the other hand, is expecting a fall of 2.8% in pension expenditure from 14.9% to 12.1% over the same period. Although France currently spends more on pensions, its higher birth rates should mitigate these costs.

While reform of pension systems is slow in the majority of countries, some are providing useful lessons in how to create more sustainable, inclusive systems. Markus Knell, a researcher at the Austrian Nationalbank (the central bank), believes that many European countries, including Austria, can take a leaf out of Sweden’s book. Sweden has sought to link pension contributions and payments to life expectancy. “The Swedish pension system automatically adjusts to changing demographics,” Mr Knell explains. “An increase in life expectancy leads to an automatic reduction in benefits—assuming, of course, that people do not postpone their retirement.”

Nudged towards a new contract

Notwithstanding these changes, there is a growing recognition by many of the need for a broader, more collective approach to the social contract: how to meet the financial needs of the ageing while assuring dignity and satisfying roles.

Social policies, for example, can “nudge” workers to save more for their retirement—using ideas from behavioural economics, such as positive reinforcement and indirect suggestions, to try to coax people to save more. “I'm a great believer in nudging,” says Keith Ambachtsheer, director emeritus of the Rotman International Centre for Pension Management at the University of Toronto (ICPM). “You can see inertia everywhere. Nudges, I think, make total sense.”

Yearning to retire

Most experts believe that one of the best ways to reduce the overall pension burden is for people to work longer. Workers get paid for the extra work, economic output is boosted, and the cost of pensions falls. “We must better communicate the message that working longer and contributing more is the only way to get a decent income in retirement,” notes the OECD secretary-general, Angel Gurría, in his organisation’s report Pensions Outlook 2014.

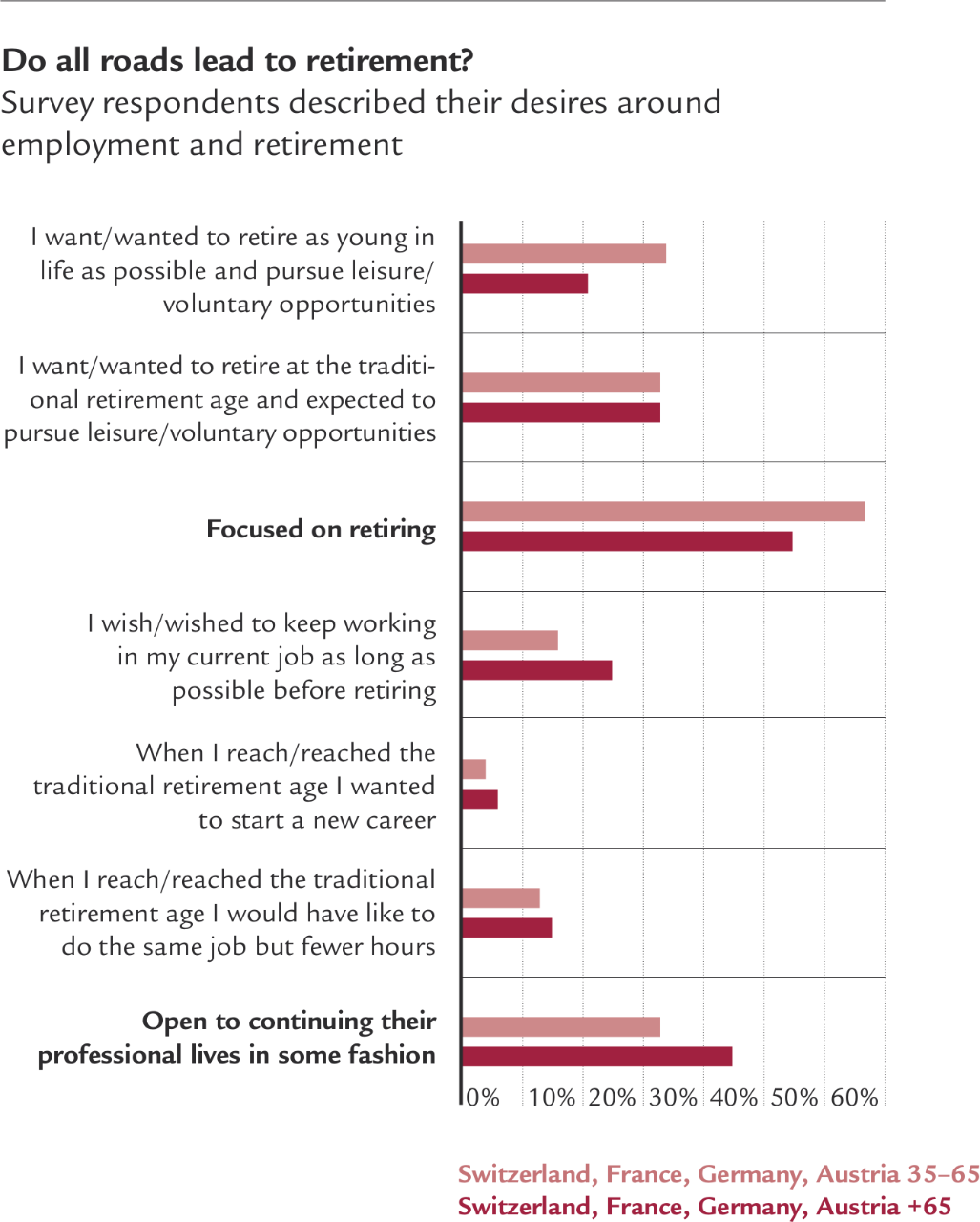

As we have seen, much of the general public recognise a need for change, but many would prefer that someone else do the changing. The results of the EIU survey show that two-thirds of respondents wish to retire at the traditional retirement age. This attitude is consistent across all countries, indicating that regardless of the matter of longevity, respondents wish to adhere to the established practice of retiring in their mid-60s.

However, the survey suggests that those who have already reached this age can have a change of heart once retired. This change of attitude is something that policymakers could potentially work with if they are to create enticing reasons for people to remain in the workforce. Collectively, one-third of workers express an interest in continuing their professional careers or reinventing them in some fashion. This substantially exceeds the share of older workers currently employed in all four countries surveyed.

In the Swiss canton Aargau an initiative called Campaign 50+ has promoted the benefits of hiring older workers. The programme showcases posters of employees over the age of 50, but rather than specifying their ages, the poster details years of work experience instead. Between 2013 and 2014 there was a 52% increase in the number of workers aged 50+ who found employment in Aargau. Valentin Vogt, president of the Swiss Employers’ Association, says that in order to sustain an older demographic more needs to be done on this issue and that there is “a need to make sure that we use the potential that we have in the country, and part of that are older employees”.

Clearly, there is a role for companies here as well. Research conducted for the European Commission’s Directorate-General for Employment, Social Affairs and Inclusion investigated why people over 55 stop working. This revealed that the most commonly cited factors were lack of opportunities to retire gradually, exclusion from training, and not being viewed positively by employers—all facets of employment that companies can change.

Building a virtuous cycle

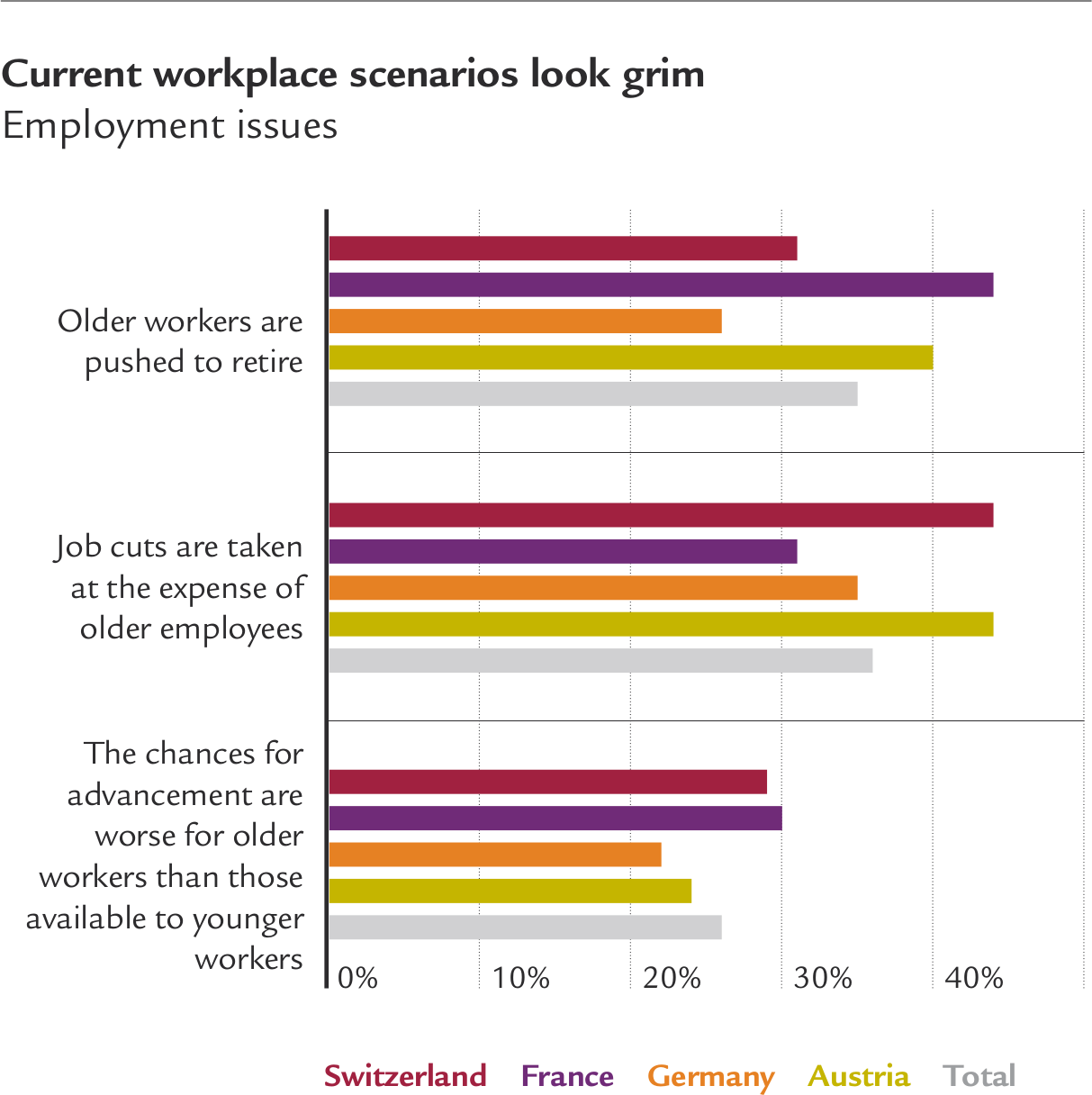

Employers score poorly on policies for older workers, according to the findings of the EIU survey. Older workers being pushed into retirement, job cuts at the expense of older workers and limited chances to advance were three clear issues raised by respondents, both those over 65 and their younger peers. If policymakers are to increase the number of workers remaining in employment for longer, changes will need to be made to keep working opportunities attractive.

Mr Knell of the Austrian Nationalbank points to the possibility of a virtuous circle: “Once you see that your co-workers and friends are working longer, then you might also change your own behaviour.” However, it will take a broader, more substantive approach to convince people that working for longer is more desireable than being able to travel, control one’s leisure time or spend more time with one’s family. There are ample opportunities to promote the benefits of staying in employment, both for the individual and for society, to younger generations as well as those close to retirement. The key lies not in forcing work on those aiming to retire but in further unlocking opportunities for those seeking to continue their professional lives.

Written by