Whether it’s cash stuffing, the penny challenge or tracking your expenses with pen and paper, old-school methods can make saving and budgeting more tangible again in the digital age. Below we present the best tips.

1

The Kakebo method: budget the Japanese way

The first step to saving successfully is realistic budget planning. The Kakebo method has proved particularly effective. For more than a century, this Japanese method of budgeting has been teaching people how to get a better handle on their expenses. All you need for this method is a household budget book in which daily expenses are recorded and broken down into categories: basic needs (e.g. rent or groceries), culture (e.g. books or hobbies), optional items (e.g. restaurant visits or shopping), and unexpected expenses (e.g. doctor’s bills or birthday gifts). Then you review your budget at the end of each month, based on the following questions: how much money do I have available? How much money would I like to save? How much money do I actually spend? And how can I reduce my expenses? This method provides a detailed overview of your actual cash flow and thus ensures a more mindful approach to money.

2

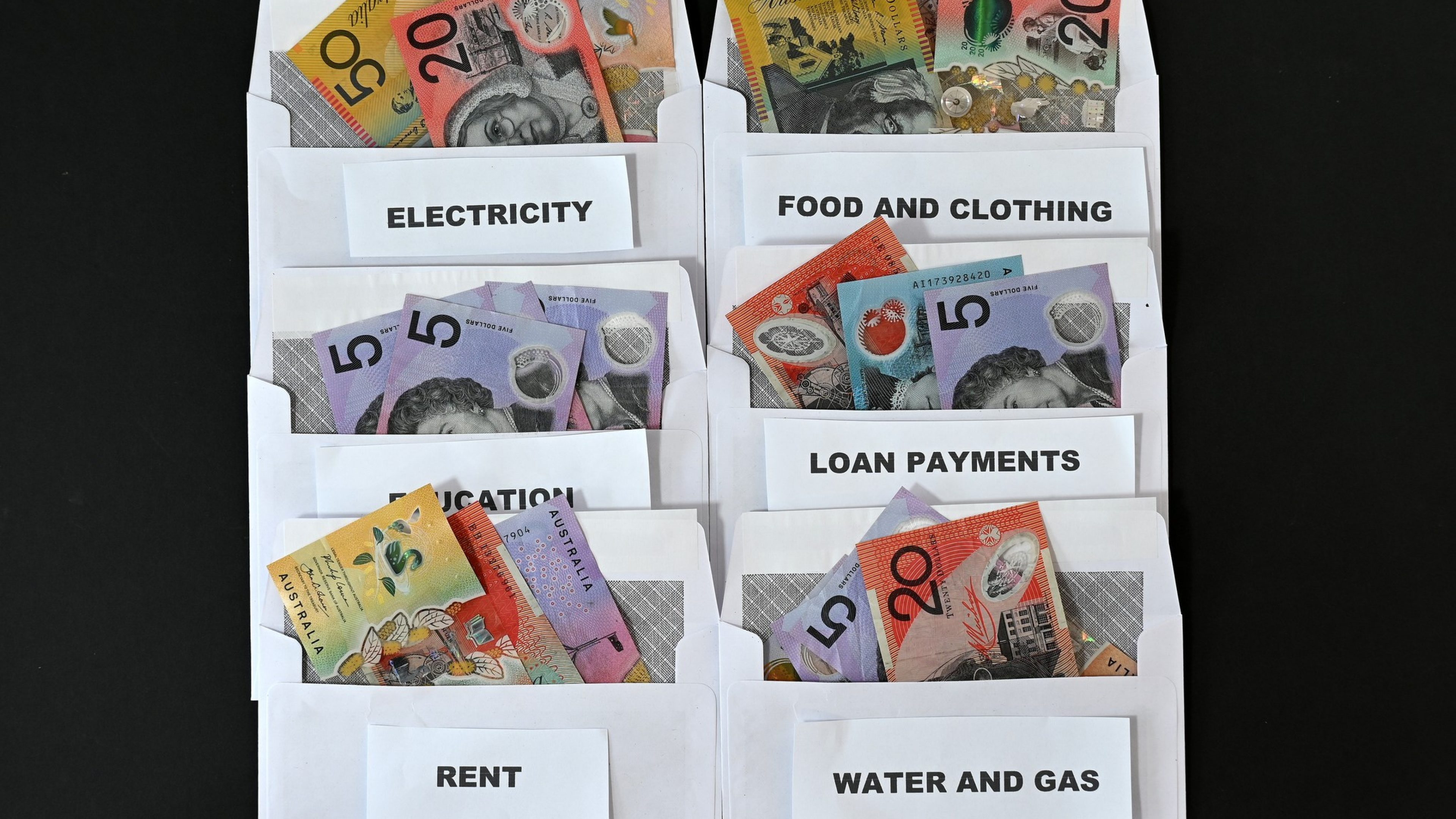

Cash stuffing: never live beyond your means

One simple life hack for saving money is the envelope method, also known as “cash stuffing”. You withdraw your entire monthly income in cash at the beginning of each month – yes, everything! – and put it into different envelopes according to your budget categories: one for fixed costs such as rent and utilities, one for variable costs such as food and clothing, one for leisure activities and one for emergencies. The advantage of this approach is that you never live beyond your means. And the money left over at the end of the month can be used to save or invest.

3

Penny challenge: micro-saving for children (and adults)

The penny challenge is a popular way to introduce the concept of saving money to young people. On the first day, your child puts a cent in the piggy bank, on the second two cents, on the third three cents, etc. After 365 days they have saved 667.95 euros. It’s best to join in, because the method works for adults too, for example to save up for holidays. For the Swiss: if you start with 5 centimes and continue with 10, 15, 20 etc., you will have saved a total of CHF 3,339.75 after 365 days.

4

50% rule: always put half in savings

For a financially self-determined future, it is crucial to set aside money regularly and stick to your savings plan. These lessons can be taught to children with the 50% rule. The idea: half of any money the child receives is always saved until they turn 18. Whether received as a gift or earned independently, 50% of all “income” is deposited into a savings or investment fund account. The effect is greatest if the child makes the deposit on their own. This way, they not only have a nice starting sum for their adult life, but ideally they have also internalised the value of long-term saving and investing.

5

10-minute 30-day rule: prevent impulse buying

An effective strategy to save money when shopping is the 10-minute-30-day rule. It helps to avoid impulse buying. For smaller purchases starting at 30 euros or Swiss francs, you should take 10 minutes to think about it – and leave the shop or online shop while you mull over your decision. For larger purchases of more than 300 euros or francs, it is advisable to wait 30 days. The reflection period helps to determine whether you actually need the purchase or whether you can do without it. This approach can significantly reduce your expenses.

6

The pre-set effect: outsmart yourself

As we all know, people do not always make rational and wise decisions. This same applies to saving money. That is why we sometimes have to outsmart ourselves, as behavioural economist and Nobel laureate Richard Thaler has researched. One proven measure is having default rules, or pre-sets, that automate our financial behaviour. In specific terms, this means you should set up automatic debits from your salary account and transfer a fixed amount to your savings or investment account at the end of each month. The advantage of this approach? You don’t have to think about your savings plan anymore, and you won’t even be tempted to throw it overboard at short notice.

7

SMART method: Set specific savings targets

Psychologically, goals are important – including when it comes to saving. And the more specific the goals, the more motivating they are. A good trick for your personal savings plan is to apply the SMART method, developed by psychologist Edwin Locke. SMART stands for specific, measurable, achievable, realistic and time-bound. Always check whether your savings targets meet these five conditions. The more consistently you take them into account, the more likely you are to reach your savings goals, according to Locke.

8

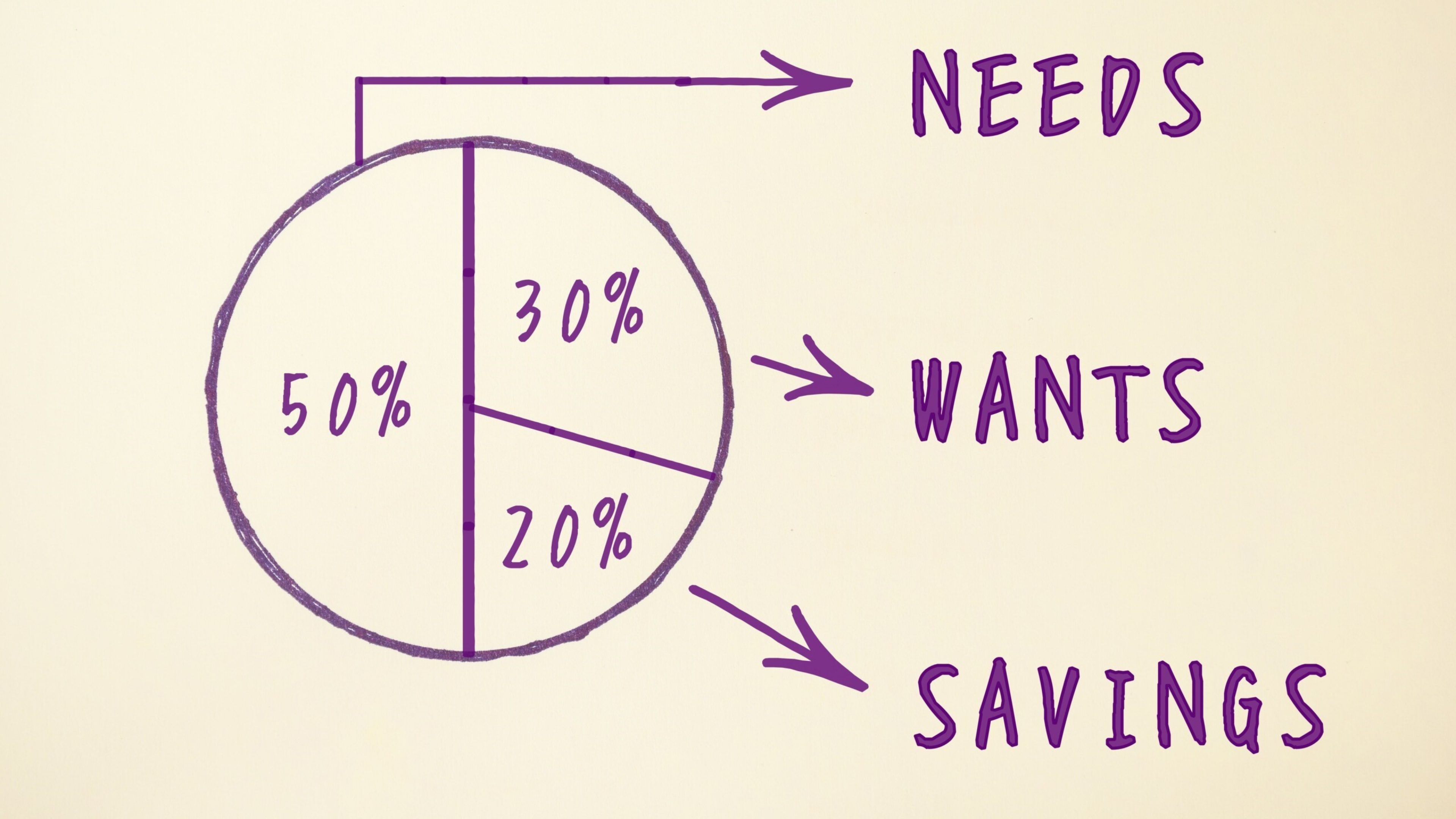

The 50–30–20 rule: a classic for long-term saving

The 50–30–20 rule is particularly suitable for accumulating assets over the long term and funding your retirement. Created by US Senator and Harvard Professor Elizabeth Warren, it helps people structure and keep track of their spending. The trick is simple: you divide your monthly household income into three categories. 50% for fixed costs (rent, internet, food, etc.), 30% for leisure (clothes, cinema, travel, etc.), and the remaining 20% for saving (or paying off debt). It is advisable to keep separate accounts for each of the three areas. That way, you won’t be tempted to use the money for other purposes.

9

“No coffee to go” rule: small sacrifices are worthwhile

Even small expenses can put a lot of strain on your budget, which is illustrated by the “no coffee to go” rule. Let’s say you buy yourself a coffee every morning on your way to work, spending between 15 and 20 euros/ francs a week. If you forgo this expense and save the money instead, you will have around 10,000 euros/francs more in your account after 10 years.

10

The dice challenge (or screen time discipline): make saving fun

Studies show that the probability of reaching a savings target increases by 20% if the wealth can be accumulated in a playful way. Money-saving challenges are an entertaining spin on this, with the “dice challenge” probably being the most fun. You roll two dice each week and put the numbers you roll into your savings account. You can decide for yourself how many zeros you add to the end. The higher the stakes, the higher your “winnings”. Either way, you’ll have a nice amount of money after a year.

Playful approaches to saving money can also be combined with other New Year resolutions – for example, reducing your screen time. To do so, check your weekly screen time on your smartphone once a week and set aside one euro or franc for every full hour. Assuming your screen time is 27 hours per week (worldwide average), that’s around 1,400 euros or francs per year. At the same time, this means that you spend around 59 days a year – almost two months – on your smartphone. Ideally, you can reduce your screen time – and use the money you save to finance theatre or spa visits.